Author: Owen Rosen

Michigan Auto Insurance Reform (PIP) Part 1

You’ve probably heard that the Michigan legislature recently passed significant changes to our no-fault auto insurance laws. You may have questions as to what the changes mean for you and your family’s insurance plan. We have answers and will continue to publish updates over time.

Most of the changes do not take effect until July of 2020 but the first change is effective now. The reforms revolve around the Personal Injury Protection (PIP) portion of the no-fault policy. In Michigan, PIP basically means medical payments required as a result of car accidents. The coverage is expansive though and can cover things such as renovations to a primary residence to make them accessible to the disabled, physical therapy, transportation to medical appointments, etc.

The first amendment clarifies the definition of the insured for PIP coverage to:

•the named insured(s)

•the named insured(s) spouse

•resident relatives (must be both a blood/legal relative and a permanent resident at the primary address)

Common situations that this will directly impact would be a boyfriend/girlfriend, fiance, children that no longer reside in the household of the insured parents, etc. Those individuals, if uninsured, would be limited to $250,000 medical coverage through an entity called the Michigan Assigned Claims Plan. Regular coverage has no dollar limit.

If you think you might be affected by these changes (whether you are insured by PKIG or not) please give us a call and we’ll walk you through what you need to know. If you have any other questions, please call for clarification. Stay tuned to this space and our social media for further updates and crucial information.

(248) 682-7445

info@philkleininsurance.com

Should you convert your term life policy?

Should you convert your term policy?

Term life insurance makes sense for many of us. Specifically, this coverage option provides low-cost protection to the loved ones who would be affected by the loss of your income and other household contributions.

But what happens if you’re approaching the end of the pre-decided term with less financial security than you thought you’d have by now?

Find out more about a step you can take to help keep your family safe:

When does converting your policy make sense?

Medical bills, a job loss and other circumstances sometimes limit wealth accumulation. Thankfully, an easy solution — converting your term policy to whole life — might be within reach if your timing is right.

How does a conversion work?

Most term policies provide a window to convert before your term expires or before you reach a certain age. You typically won’t have to qualify medically, which may get you a lower rate on whole life.

What are some of the long-term benefits of converting your term policy?

A whole life policy lasts for your entire life (as long as you pay the premiums), allowing you to leave money to heirs or charity. Whole life can also support a lifelong dependent, such as a sick or disabled child or spouse. It can also be a tool for mitigating estate taxes.

You may also borrow against the accumulated cash value of a whole life policy for any reason. Just note that policy loans accrue interest, and loans outstanding at death reduce the policy’s death benefit.

What else should you know?

Whole life tends to be more expensive than term because of the additional policy benefits and guaranteed payout. Partial conversion can be a more affordable option.

Have questions? Please reach out to discuss your options if you’re concerned your term policy may be too short.

Polar Vortex 2019: Preventing & Thawing Freezing Pipes in Michigan

Why Pipe Freezing is a Problem

Why Pipe Freezing is a Problem

Water has a unique property in that it expands as it freezes. This expansion puts tremendous pressure on whatever is containing it, including metal or plastic pipes. No matter the strength of a container, expanding water can cause pipes to break.

Pipes that freeze most frequently are:

Pipes that are exposed to severe cold, like outdoor hose bibs, swimming pool supply lines, and water sprinkler lines.

Water supply pipes in unheated interior areas like basements and crawl spaces, attics, garages, or kitchen cabinets.

Pipes that run against exterior walls that have little or no insulation.

How to Protect Pipes From Freezing

Before the onset of cold weather, protect your pipes from freezing by following these recommendations:

Drain water from swimming pool and water sprinkler supply lines following manufacturer’s or installer’s directions. Do not put antifreeze in these lines unless directed. Antifreeze is environmentally harmful, and is dangerous to humans, pets, wildlife, and landscaping.

Remove, drain, and store hoses used outdoors. Close inside valves supplying outdoor hose bibs. Open the outside hose bibs to allow water to drain. Keep the outside valve open so that any water remaining in the pipe can expand without causing the pipe to break.

Add insulation to attics, basements and crawl spaces. Insulation will maintain higher temperatures in these areas.

Check around the home for other areas where water supply lines are located in unheated areas. Look in the garage, and under kitchen and bathroom cabinets. Both hot and cold water pipes in these areas should be insulated.

Consider installing specific products made to insulate water pipes like a “pipe sleeve” or installing UL-listed “heat tape,” “heat cable,” or similar materials on exposed water pipes. Newspaper can provide some degree of insulation and protection to exposed pipes – even ¼” of newspaper can provide significant protection in areas that usually do not have frequent or prolonged temperatures below freezing.

Consider relocating exposed pipes to provide increased protection from freezing.

How to Prevent Frozen Pipes

Keep garage doors closed if there are water supply lines in the garage.

Open kitchen and bathroom cabinet doors to allow warmer air to circulate around the plumbing. Be sure to move any harmful cleaners and household chemicals up out of the reach of children.

When the weather is very cold outside, let the cold water drip from the faucet served by exposed pipes. Running water through the pipe – even at a trickle – helps prevent pipes from freezing.

Keep the thermostat set to the same temperature both during the day and at night. By temporarily suspending the use of lower nighttime temperatures, you may incur a higher heating bill, but you can prevent a much more costly repair job if pipes freeze and burst.

If you will be going away during cold weather, leave the heat on in your home, set to a temperature no lower than 55° F.

How to Thaw Frozen Pipes

If you turn on a faucet and only a trickle comes out, suspect a frozen pipe. Likely places for frozen pipes include against exterior walls or where your water service enters your home through the foundation.

Keep the faucet open. As you treat the frozen pipe and the frozen area begins to melt, water will begin to flow through the frozen area. Running water through the pipe will help melt ice in the pipe.

Apply heat to the section of pipe using an electric heating pad wrapped around the pipe, an electric hair dryer, a portable space heater (kept away from flammable materials), or by wrapping pipes with towels soaked in hot water. Do not use a blowtorch, kerosene or propane heater, charcoal stove, or other open flame device.

Apply heat until full water pressure is restored. If you are unable to locate the frozen area, if the frozen area is not accessible, or if you can not thaw the pipe, call a licensed plumber.

Check all other faucets in your home to find out if you have additional frozen pipes. If one pipe freezes, others may freeze, too.

Tips by the American Red Cross

7 ways to make the most of your health benefits

We all know that health insurance is a significant monthly expense. But it’s worth the cost, as it enables access to the care you need and reduces your risk of medical debt.

Here’s how to make sure you get the most for your money this year.

1. Don’t skip preventive care. You may have access to an annual physical, vaccines and screenings at no cost before meeting your deductible. Preventive care can keep potentially serious health problems at bay.

How To Know When You’re Ready to Retire

Many workers look forward to retirement and the new changes and opportunities it brings; but, some might struggle to determine when they are ready to retire. There’s no exact science or magic number to determine the right time to retire. Instead, attention to retirement savings and creating a plan for what to do during retirement may help you better understand when you are both financially and emotionally ready for retirement.

Financial Retirement Readiness

According to a 2018 study of over 2,000 working Americans ages 40-70, about one-fifth of respondents were financially unprepared for retirement.(1) While many retirees rely on Social Security benefits to help fill savings gaps, currently, Social Security benefits only cover approximately 40 percent of an average worker’s pre-retirement income.(2) In addition to personal savings and Social Security benefits, other sources to supplement retirement income include individual retirement arrangements (IRAs), employer-sponsored retirement plans (401(k) plans, pensions, profit sharing plans, etc.) and fixed indexed annuities.

Everyone has different financial needs in retirement. When considering whether you are ready to retire, evaluate your financial strength to see if you are in a position to stop working. A retirement calculator can help you establish a retirement savings goal by comparing your income and current savings with your age and anticipated expenses. Various retirement calculators are available online, free of charge.

An additional way to help gauge financial readiness is to examine how retirement costs will affect your nest egg. Some retirement costs to consider may include:

*Healthcare

*Housing

*Debt

*Extra expenses, such as traveling

According to the Bureau of Labor Statistics data, older households typically spend an average of $49,279 a year on living expenses, including food, housing, clothing, transportation, healthcare and entertainment.(3) Having a plan in place for how to pay for expenses may help you feel more confident in your decision to retire.

Emotional Retirement Readiness

While meeting financial goals is an important part of retirement planning, an often forgotten aspect is emotional readiness. For many, working provides a sense of validation, in addition to other psychological benefits, such as a daily structure and social interaction. Because of that, retiring may present a sense of loss for some and be a risk for depression.(4) Retirement is a major change, with emotional implications, that shouldn’t be done on a whim. Consider creating a list of your goals for retirement. Do you want to travel? Spend more time with your grandkids? Start a new hobby? Work part time? Move to a new city? After you’ve established your goals, create a plan to achieve those goals.

Here are some other ways to better prepare for the emotional side of retiring:

*Create a plan for how you will spend your days in retirement

*Establish a retirement bucket list

*Find or create an emotional support system of friends and family

*Pursue a new hobby or consider a part-time job as a bridge from working to full retirement(4)

Deciding when to retire can be a complex decision with many factors contributing to retirement readiness. Ultimately, the only person who truly knows when you are ready to retire is you. Paying attention to both financial and emotional milestones and defining retirement goals can all help you in making the decision to retire.

If you need professional guidance or have questions, please call us today at (248) 682-7445 or email owen@philkleininsurance.com

Footnotes

Footnote 1 Indexed Annuity Leadership Council, “The State of America’s Workforce: The Reality of Retirement Readiness” 2018↩

Footnote 2 Social Security Administration, “Learn About Social Security Programs” ↩

Footnote 3 Bureau of Labor and Statistics, “A Closer Look at Spending Patterns of Older Americans” 2016↩

Footnote 4 US News and World Report, “Can Retirement Be a Depression Risk?” 2017

Ready for your life insurance health exam?

When you’re applying for an individual life insurance policy, you’ll usually need to complete a simple medical exam administered by a paramedical professional. However, at PKIG we can offer up to $1 million in coverage without a medical exam in many cases. If you do need to complete the exam, follow these steps to prepare for your exam so you can minimize your chances of inaccurate test results and set yourself up to receive a fair rate on your policy.

When to Eat

Read and follow your pre-exam directions. If you’re supposed to fast for eight to 10 hours, make sure you do. Fasting properly means you won’t get a false positive on blood glucose tests for diabetes or artificially high cholesterol levels because of something you ate. Don’t even drink black coffee the morning of, as caffeine can increase your blood pressure.

Tip: If you accidentally eat something before your test, ask the examiner if you need to reschedule.

What to Eat

You may also want to pay attention to what you eat and drink for at least 24 hours beforehand. Avoid alcohol, skip salty foods and drink plenty of water. Consuming too much alcohol, too much sodium or not enough water can throw off test results for liver and kidney function as well as urine concentration. It’s also easier to give blood when you’re well-hydrated.

Exercise Considerations

Finally, avoid tough workouts in the 12 to 24 hours before your exam, as heavy exercise can lead to urinalysis results that may suggest kidney problems and high blood pressure. But a light workout, like a walk, may be a good idea to help you get a good night’s sleep. And, being properly rested can possibly improve your test results by decreasing anxiety and lowering blood pressure.

Thinking over your life insurance options? Reach out if you have any questions. 248-682-7445 or owen@philkleininsurance.com

How To Avoid Six Situations That Can Destroy A Business

1. “I KNOW WHAT MY BUSINESS IS WORTH”

•Have you ever had your company value appraised by an outside resource?

•Has that appraisal been done within the last three years?

•Do you have a Buy/Sell agreement? •Is it funded?

•Has it been reviewed within the last three years?

•Do you know where your Buy/Sell agreement is kept?

2. “I’M TOO BUSY RUNNING THE COMPANY”

•Do you have a will? •A trust?

•Is it up to date?

•Do you have a plan to retain key employees if something happens to?

•Has your Trust & Estate Plan been reviewed in the last three years?

•Have you identified and written down your trusted advisors?

3. “THAT’LL NEVER HAPPEN TO ME”

•Do you have a succession plan in place?

•Have you involved both key employees and family members in your succession planning?

•Does your succession plan have a provision for disability?

•Have you identified or written down who you want to run the company?

•Do you have disability buy-sell overhead expense coverage?

4. “THERE’S PLENTY OF TIME FOR THAT”

•Do you know when you want to retire? •How much income will you need?

•Do you want to be running the company full-time, five years from today?

•Do you know how much control in the business you must maintain in order to secure your retirement income?

•Have you explored financing opportunities for key employees to buy the company in the future?

5. “MY BUSINESS IS MY RETIREMENT”

•Do you have a retirement vehicle other than your business?

•Is 25% or less of your business assets a part of your retirement plan?

•Will your retirement funding come from more than four sources?

•Have you had your retirement income projected/analyzed to identify shortfalls?

•In the past year, have you spent more than one hour planning for retirement?

6. “YOU CAN’T BEAT UNCLE SAM”

•Do you have a TEAM of financial advisors working with you?

•Are you proactively planning to deal with changes in the tax laws?

•Will any sources of your retirement income be received tax free?

Questions? Concerns? Call Owen Rosen at (248) 682-7445 today or email owen@philkleininsurance.com

Is Your Employer-Provided Life Insurance Coverage Enough?

Is the life insurance you’re getting through your employer enough to take care of your family? And are you paying too much for that coverage? A healthy 50-year-old male could save nearly 80% on premiums in the first year alone by switching from an employer-provided term life insurance policy to an individual one, according to the National Association of Financial Planners. Young, healthy employees might also be better off with individual coverage, since they can lock in low rates for decades.

But many companies pay for some amount of life insurance for their workers; they also allow workers to purchase more coverage for themselves and their spouses at a low cost and with no medical exam. As a result, many families obtain all of their life insurance through an employer. If you make $75,000 per year, your employer might provide $75,000 or $150,000 in coverage at little or no out-of-pocket cost to you, and the premiums will come straight out of your paycheck. This way, you’ll never miss the money or worry about paying the bill. And even if you’ve had less-than-perfect health, you’ll qualify for just as much coverage as your co-workers. That all sounds enticing, but there are several potential problems with obtaining life insurance through work.

Problem 1: Your Employer May Not Offer Enough Life Insurance

While basic employer-provided life insurance is low-cost or free, and you may be able to buy additional coverage at low rates, your policy’s face value still may not be high enough. If your premature death would be a financial burden to your spouse and/or children, you probably need coverage worth five to eight times your annual salary. Some experts even recommend getting coverage worth 10 to 12 times your annual salary. PKIG can help determine how much you need based on your goals.

Another shortcoming? Salary doesn’t take into account bonuses, commissions, other sources of income, and the value of other benefits such as medical insurance and retirement contributions.

Your employer’s group life insurance might be sufficient if you’re single or if you have a spouse who isn’t dependent on your income to cover household expenses and you don’t have children. But if you’re in this situation, you might not need life insurance at all.

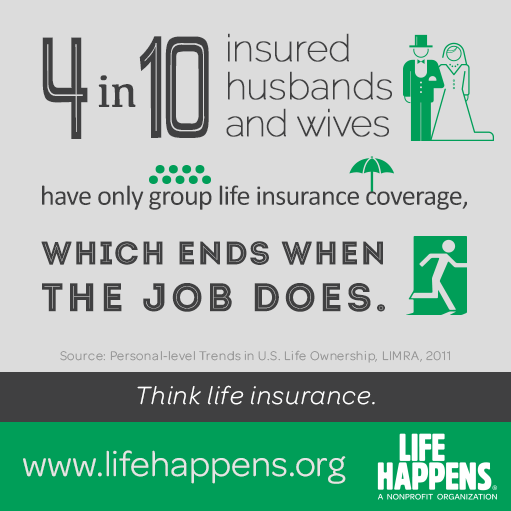

Problem 2: You’ll Lose Your Coverage If Your Job Situation Changes

As with health insurance, you don’t want gaps in your life insurance coverage because you never know when you might need it. Most workers who get coverage through work don’t know where their life insurance will come from if they change jobs, are laid off, their employer goes out of business or they switch from full-time to part-time status. You usually won’t be able to keep your policy in these scenarios. Lack of portability can be a problem if you aren’t going directly to another job with similar coverage and aren’t healthy enough to qualify for an individual policy. Some policies do allow you to convert your group policy to an individual one, but it will likely become much more expensive. If you’re losing your coverage because you were laid off, the premiums might be unaffordable.

Problem 3: Coverage Gets Tricky If Your Health Declines

Another problem arises if you’re leaving your job because of a health problem. If a medical condition forces you to leave your job, it’s unlikely that you would be able to qualify for life insurance at that time. Needless to say, that’s the time your family would need the coverage most.

Even if your health problems aren’t significant enough to stop you from working, they might limit your employment options if you only have life insurance through work.

Problem 4: Your Plan Doesn’t Provide Enough Coverage for Your Spouse

While your employer’s benefits package probably provides health insurance for your spouse, it won’t always provide life insurance for him or her. If it does, the coverage may be minimal—$100,000 is a common amount, and that doesn’t go far when you lose your husband or wife unexpectedly.

Couples often assume the family will only suffer economic hardship if the primary breadwinner dies and many workers fail to adequately insure their spouses. The death of a non-working or lower-earning spouse can certainly impact their partner’s income. You probably aren’t going back to work on Monday if you lose your spouse over the weekend. How much paid time off do you have to cover an extended leave? Plus, you must now pick up the slack with day care or carpooling – hours can be cut back – there won’t be enough time to properly grieve and survivors are often depressed which lowers productivity.

Problem 5: Employer-Provided Life Insurance May Not Be Your Cheapest Option

Even if you can get all the life insurance you need for both you and your spouse through your employer, it’s a good idea to shop around to see if your employer’s supplemental insurance really offers the best value for the money. You’re more likely to find a better rate elsewhere the younger and healthier you are. Also, unlike the guaranteed level-premium life insurance you can purchase individually, which costs you the same amount every year for as long as you have the policy, the policy provided by your employer tends to get more expensive as you age.

Employer provided coverage tends to increase in price after age 35 and typically increases every year or five years. Once you reach age 50 the policy can often become much more expensive and usually unaffordable closer to retirement age.

The Solution

While there’s no reason not to take advantage of any free or inexpensive insurance your employer offers, it probably shouldn’t be your only source of life insurance, nor should most people rely heavily on the supplemental life insurance they can get through work. The solution to each of the problems described above is to purchase some or all of your life insurance directly through an individual term policy. You might need to purchase as much as 80% of your life insurance on your own to have enough and to make sure you’re covered at all times and under all circumstances.

If you don’t think you qualify for individual life insurance, it’s important to actually find out. Underwriting standards have changed considerably over the past ten years or so. Also, if you work with an Independent Agency like PKIG your chances of approval will be dramatically higher. Captive insurers such as State Farm or Allstate typically have much stricter underwriting standards which lead to higher premiums and more frequent declinations on average. The most affordable solution is to buy the most insurance you can afford at the youngest age, since, as you age, the chance of acquiring an illness goes up, and with illness comes more expensive premiums, if you can qualify at all.

The Bottom Line

You need enough life insurance to cover all your debts and support your dependents. “Enough” includes paying off your credit cards, car loans and mortgage, paying for your children’s education, and making sure your spouse will have the financial means to take care of him or herself and your children. In a time of grief, the last thing you want is to leave your loved ones with another major life upheaval such as having to change jobs or schools because of financial strain, so take a close look at whether the life insurance you’re getting through work is the best way to provide for your loved ones.

Get instant quotes on top-rated life insurance coverage here in less than 30 seconds or call (248) 682-7445 for more information today.

The Ins and Outs of General Liability Coverage: What’s Covered – And What’s Not

As a small business owner, you have a lot on your plate. From accounting, to marketing and sales, to product development and inventory — the to-do list can seem never ending. That’s why it’s no surprise that details like liability insurance can so easily slip through the cracks, leaving your business financially vulnerable.

Unfortunately, nearly anyone your business interacts with can make claims against you. And without the right insurance protection, these claims could cripple your operation.

What General Liability Insurance Covers

General liability (GL) coverage can be part of a standalone policy or can be part of a business owner’s policy (BOP). This coverage safeguards your business’ finances and reputation in the event a customer or third party takes legal action against you or your employees.

The following are types of claims covered by a GL policy:

Bodily injury: If a third party is injured at your place of business (or as a result of work performed away from your business), your GL policy would cover costs, including medical expenses, lost wages, and any court-awarded compensation or out-of-court settlements.

Property: If your business’s actions result in damage to someone else’s property, your GL policy will cover costs to repair the damage. This applies to real estate, equipment, and supplies, as well as compensation for loss of use during the time it takes for the damaged property to be repaired or replaced.

Personal and advertising injury: If your business causes nonphysical damage to a third party through advertising tactics or other activities, your GL policy will cover these damages. However, coverage does not apply if your business intentionally makes a false statement knowing it will cause harm.

Additionally, if a lawsuit is filed against your business for a covered loss, your GL policy will also cover the legal costs to defend you in addition to your policy limits, including attorney fees and court costs.

GL coverage safeguards your business’s finances and reputation in the event a customer or third party takes legal action against you or your employees.

What General Liability Insurance Doesn’t Cover

GL coverage does have limits — both in dollar amounts and types of situations covered. This depends on a number of factors, including your specific industry and your business’s exposure to visitors and clients.

However, there are a few limits that apply to businesses across the board. GL does not cover the following types of damages:

Workplace injuries: GL normally doesn’t cover workplace injuries to employees. Instead, you’ll need workers compensation coverage, which is legally required by most states.

Damage to your own property: GL covers damages to other parties’ property, but it doesn’t cover your business’s property. Instead, you’ll need a business owner’s, inland marine, or commercial property policy.

Intentional damage: Damage done purposefully or maliciously is not covered under a GL policy.

Damage to client property in your care: GL does not cover damage to a customer’s property while it is in your care. Inland marine and other property coverages can provide this type of protection.

Professional mistakes: Mistakes resulting in a loss aren’t covered by GL. For instance, if your business misprints 10,000 books, general liability coverage won’t reimburse you for the cost of reprints. However, many insurers offer separate policies for businesses that require professional liability protection.

Damage to vehicles: This protection requires a commercial auto policy.

While general liability insurance won’t cover every incident and expense your business might face, it can protect your business from claims brought against you by third parties — and it’s a relatively inexpensive way to create peace of mind.

Contact us today at (248) 682-7445 or info@philkleininsurance.com for more information.